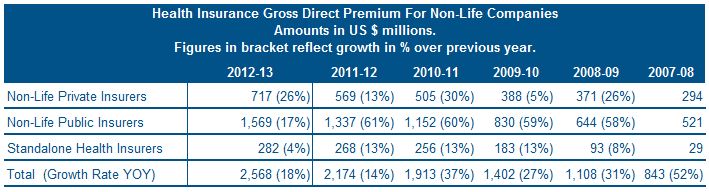

The health insurance industry in India has come leaps and bounds since the launch of the first Mediclaim policy was enacted in 1986. It is the fastest growing segment of the Indian insurance industry, as evidenced by the fact that it makes up 30.5% of the non-life insurance segment of the Compound Annual Growth Rate since the years 2005-06. This is particularly remarkable when one considers that the non-life insurance sector has shown the highest premium growth rate amongst emerging markets. Before the year 2000, there were only four public sector insurance companies providing health products in India. Currently, there are 26 private companies providing health insurance, including five stand-alone health insurance companies.

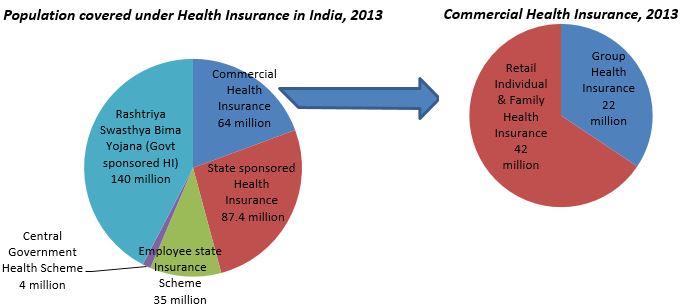

The health insurance coverage in India is split among central, state, employer, and commercial markets. Various government social schemes since 2003 have led to an enormous boost to the number of people with some form of health insurance coverage in the country. Today, nearly 370 million Indians (29%) have some form of insurance through central or state government, employer based, or private health insurance. Commercial, for-profit insurance is comprised of public and private commercial insurance companies that provide individual or family retail and group medical plans for members. State sponsored health insurance schemes offer protection to the lower income groups, and many government employee based schemes cover government, railways, and defense personnel.

While these numbers show impressive growth in the India healthcare insurance industry, the overall penetration is still low. Of the 29% Indians covered under insurance, 85% are primarily covered through social and state health initiatives. Commercial insurance is only adopted by affluent urban populations and corporate groups, while social health insurance schemes target low-income groups in both urban and rural areas. There is still a huge gap in coverage for people in the working class, lower-middle class, or those living in tier-two or tier-three cities. There is substantial opportunity to improve access to health insurance across all segments and to launch additional comprehensive health benefits for Indians.

A few government employee-based programs include inpatient benefits in addition to outpatient benefits at public healthcare facilities or within a tight private provider network. The commercial and social health schemes are primarily annual Mediclaim-type indemnity products with maximum sum assured limits and sub-limits for certain benefits. Group medical policies offered to employers/commercial players offer enhanced benefits (maternity, no pre-existing exclusions) within a maximum sum assured limit.

Recently, the main innovations in health insurance products have been a substantial increase in maximum sum assured, the introduction of life-long coverage, improved portability amongst insurers, and a wider range of benefits with accident protection, hospital cash, and critical illness riders. A few health insurers have floated disease-specific insurance coverage (e.g., cancer, cardiac surgery, and, more recently, diabetes), as well as limited outpatient attendance in the individual/family health market.

The four existing public sector companies in India continue to lead the market share, but stand-alone health insurance companies and private sector companies are making inroads. The government opened the market in 2000 and allowed a 27% stake for foreign investors that triggered the influx of foreign players into the health insurance market, providing a wider range of choices to the consumer and driving up competition.

Operationally, however, the expenses for the insurers remain higher than they are in other markets. High incurred claims ratio (ICR) is encountered in a very price-sensitive environment and profitability is limited. In the last financial year, there have been trends of rises in premiums and reduction of claim ratios and profitability by a few non-life companies, as well as one of the stand-alone health insurance companies. The experience is different across individual, family, government, and group medical policy portfolios, as well as across public, private, and stand-alone specialists. Private non-life companies have been controlling claims ratios well, however, they continue to lose out on corporate covers. Public sector companies are showing improvements but still have a long way to go.

Various factors predict a favorable outlook of the industry in the coming years. The current majority government is expected to bring in stability and catalyze economic growth. A proposed bill to increase the equity share of foreign partners to 49% will invite more foreign players to the health insurance market, which will result in better choices for members, added capability, and more competitive plans. There is interest from a range of foreign insurers who look at India as a major opportunity for growth. The government’s declared mandate to introduce universal health insurance will continue to expand focus to other low- and middle-income groups and will give further impetus to the social health insurance sector. World Bank predicts India to bring in coverage to 50% of its population under some form of health insurance plan by the year 2015.